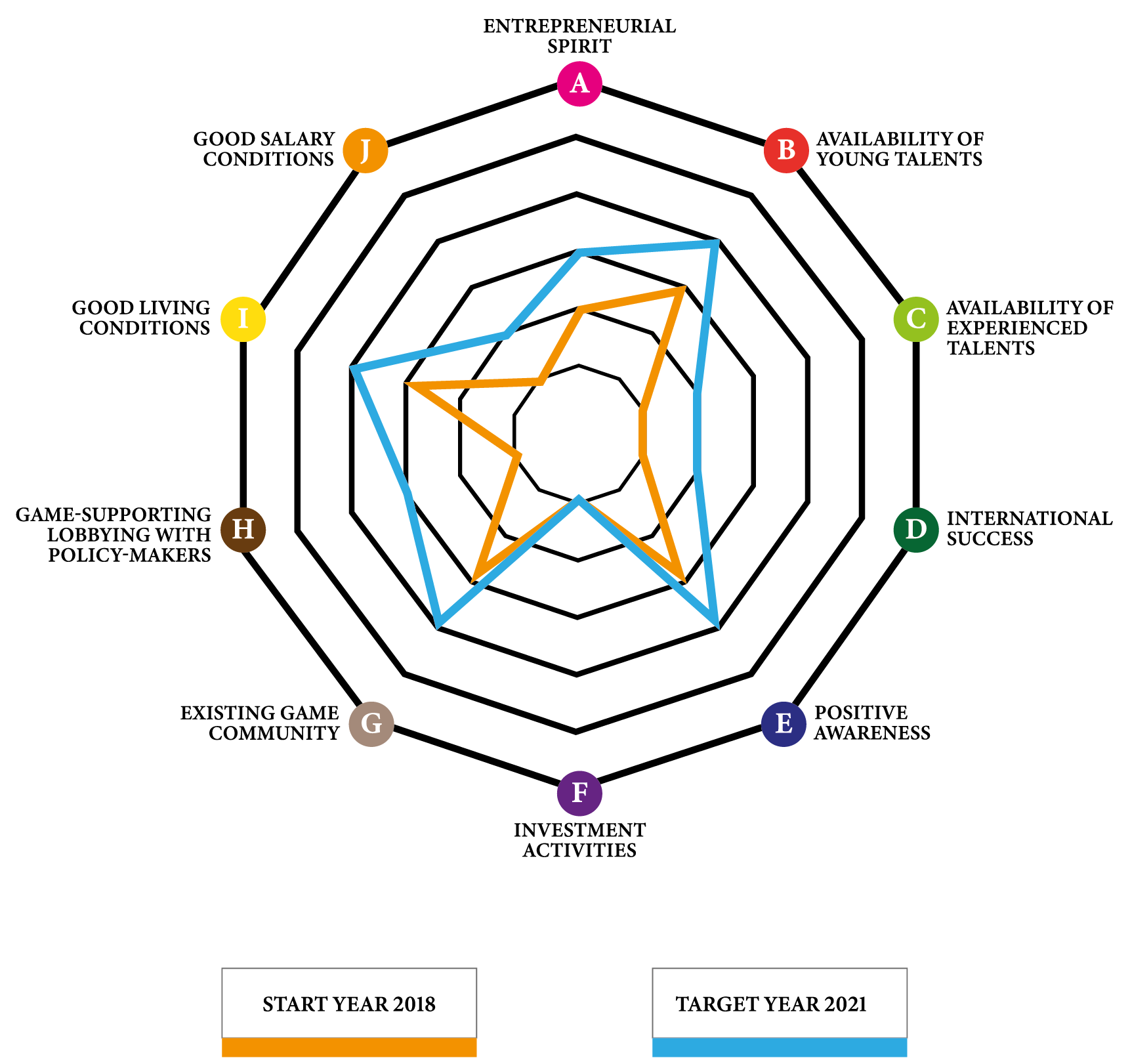

Regional Game Industry Profile Latvia

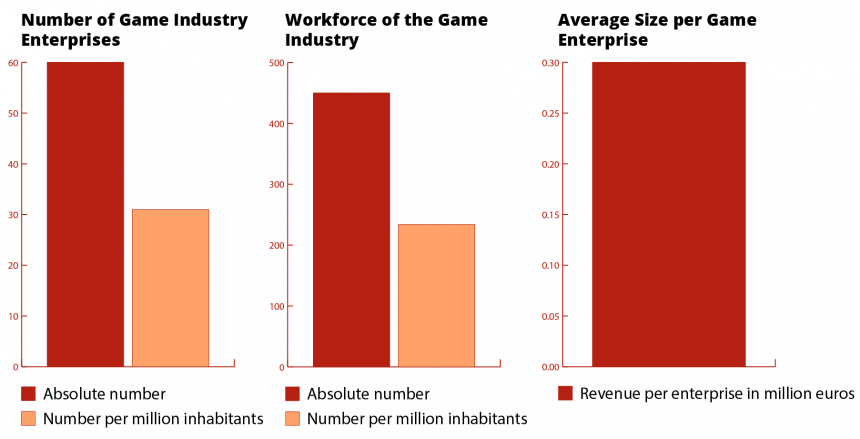

With a total of roughly 61 game companies, the Latvian game industry belongs to the young and emerging game industry within the BSR. Nevertheless, in the last 4 years there has been a slow but steady rise in both turnover and profit of game development companies registered and operating in Latvia, mainly thanks to the input of smartphone game developers.

The survey conducted at the end of 2018 by the Latvian Game Developers Association (LGDA) concluded that there are about 450 game developers in Latvia, which is slightly less than a year before. 80% of these employees are based in Riga, while the remaining 20% work in such cities as Jelgava, Ogre, Marupe, Valmiera, Rezekne, Sigulda, Kuldiga and outside Latvia – Vilnius, Parnu, Tallinn. Gender breakdown in the industry is as follows: 83% male, 17% female.

With an average of 5 employees per company, the Latvian Game Industry is dominated by small firms. In contrast to these low-ranking figures, Latvia has the largest number of technical incubators that can also cater to game start-ups. With 16 technical incubators and 3 interest/lobby associations, the Latvian Game Industry shows a high potential to offer targeted incubation support for game start-ups in order to strengthen and further build up the Latvian game industry.

Source: Latvian Game Developers Association

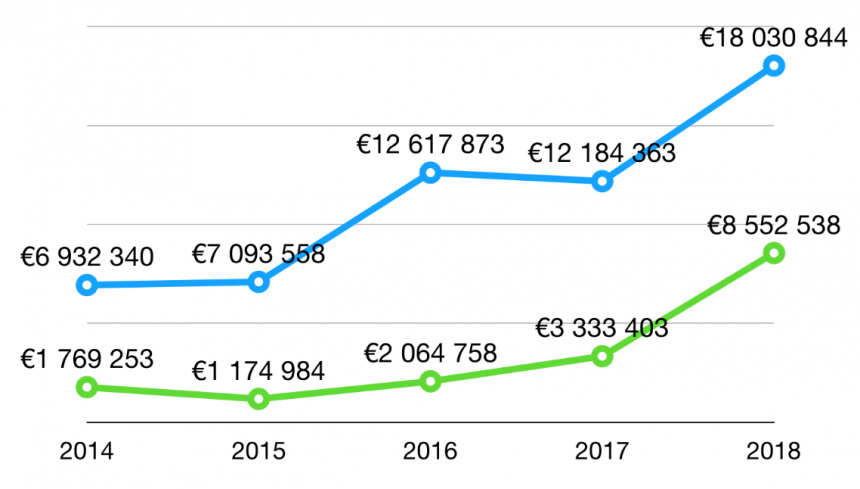

Blue: Turnover

Green: Profit

Source: Latvian Game Developers Association

The latest figures provided the by LGDA show that in 2017 the total turnover of the industry experienced a slight decrease mainly due to the fact that Suricate Games (a complex of game-development studios located in Riga), with a turnover of almost EUR 3 million, ceased operations in Latvia in 2018 and was completely liquidated in 2019. However, due to the rapid growth of Estoty (mobile games) and other companies, in 2018 these figures have increased by over 34%.

Latvian game development companies have developed around 40 games in 2018, of which almost half have been published by the developers themselves. Approximately 80% of games developed were digital games and 10% were board games.

The companies have also become more international by opening branches in different cities in neighbouring countries, but the industry is still concentrated mainly in Riga. Although the financial ratios are growing year by year, Latvia has room for improvement, as it lags far behind countries close to us, such as Lithuania, whose annual turnover in 2017 was approximately EUR 100 million, and Finland, whose turnover in 2018 was over EUR 2 billion.

| Interest/lobby associations | 3 |

| Incubators with full focus on games | 0 |

| Technical incubators that could in principle harbour game start-ups | 16 |

| Revenue | 18 m € (2018, source: Latvian Game Industry Association) |

There has also been a considerable increase in local and international activities in the Latvian game landscape, such as festivals, conferences, game jams, meet-ups, etc., indicating that the game sector is steadily gaining momentum. Another positive result is the cooperation with secondary and higher educational institutions, who as of recently are also adding game related courses to their curricula, e.g. in 2018 EKA University of Applied Sciences has introduced a study programme “Computer Game Design and Graphics” and in 2019 Ventspils University of Applied Sciences introduced a course “Introduction to Game Development”.

______________________

Status: 2020

- Latvian Video Game Association: personal communication by Ventspils High Technology Park and municipal institution “Ventspils Digital Centre”

- EKA and Ventspils University of Applied Sciences study programme webpages